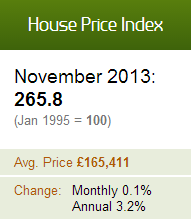

The Council of Mortgage Lenders (CML) monthly gross lending data shows that there was a 2% decrease in September to £12.9 billion. However it was 4% higher than September 2010. Yet borrowers see a drop in payments after fixed rates come to an end.

The Council of Mortgage Lenders (CML) monthly gross lending data shows that there was a 2% decrease in September to £12.9 billion. However it was 4% higher than September 2010.

The Council of Mortgage Lenders (CML) monthly gross lending data shows that there was a 2% decrease in September to £12.9 billion. However it was 4% higher than September 2010.

Gross lending for the 3rd quarter was estimated to be 15% increase on the 2nd quarter of this year and a 2% increase on last year. So all in all quite positive.

Commenting

CML chief economist Bob Pannell observes:

“Both house purchase and remortgage lending appear to have fared well in September, but this is against the backdrop of subdued levels of activity.

“However, short-term economic prospects for the UK are not favourable. The housing market is very sensitive to wider household confidence, and this seems likely to weaken over the coming months in response to the latest spike in consumer prices and headline unemployment figures.”

Borrows paying less

Further research by the CML reveals that around 1.8 million borrows whose fixed rate deals have come to an end have found themselves paying on average around £2,600 a year less then previous.

Over half of these borrowers have more than 10% equity and could potentially remortgage if they wished – which would support the demand for remortgaging to ward off any future interest rate increases.

Yet for now most borrowers are likely to play the “Wait and see” game with interest rates continuing their record lows. This is backed up by the fact that markets currently expect rates only to rise to 0.9% by the end of the year and 2% by end of 2014.

Even at this point 85% of borrowers would be paying less on the variable rate that the initial fixed rate by the end of 2012, and around 58% by the end of 2014.

CML director general Paul Smee comments:

“Most households appear to be able to absorb anticipated interest rate rises over the next few years without seeing the cost of their monthly mortgage payment rise above its original level. Many households have seen a significant windfall from reverting onto variable rates over the past few years, although this will be less true for those coming off short-term fixed rates in the near future.

“The choice of whether or not to fix, and for how long, involves taking a view about the likely direction of future interest rates, along with a personal consideration of how much rate risk is acceptable to a household. Given the economic uncertainty, it is not surprising that for the time being many of those who have reverted onto variable rates and could remortgage are choosing to wait before they decide what to do next.”

- Rental Market Sees Surge in Tenant Inquiries - May 2, 2024

- Rental Crisis: Less Than Half of Homes Ready - April 30, 2024

- Thinking Of Buying A Ground Floor Flat? Common Issues You Might Face - April 30, 2024